Updated: January 25, 2022

When Canada provinces were sent by COVID-19 pandemic to lockdown, workplaces had to ask their employees to work from home to comply with public health restrictions. Because of this millions of Canadians found themselves unexpectedly having to find space in their home to accommodate working remotely. We started to set up our work space in our bedroom, dining room, living room or even in the kitchen.

For many of us, this also resulted in spending more money on hydro and other utilities including upgrade in our internet plan to ensure that we will not lose connection while working. In its commitment to helping Canadians cope with the impacts of COVID-19 pandemic, the Government of Canada is making the home expenses deduction more accessible and easier to claim.

In November 30, thru its Fall Economic Statement, the federal government announced that they will make it easier for Canadians to claim office expenses of up to $400. Recognizing that first-time claimants may not be familiar with the existing rules and to not place unnecessary burden to employers, Canada Revenue Agency (CRA) made the home office expenses deduction available to more Canadians and is implementing some temporary changes to how employees can claim these expenses on their personal income tax return for the 2020 tax year.

These changes include:

- Employees who worked from home more than 50% of the time for a period of at least four consecutive weeks due to COVID-19 in 2020 will be eligible to claim a deduction on their 2020 income taxes for home office expenses. Two methods of claiming these deductions are available; a temporary flat rate method or a detailed method of claiming all of the expenses you paid while working from home.

- If you were not required to work from home, but your employer provided you with the choice to work at home because of the COVID-19 pandemic, provided you meet the eligibility criteria to claim home office expenses, then CRA will consider you to have worked from home due to COVID-19.

- CRA will allow employees working from home in 2020 due to COVID-19 with modest expenses to claim a flat rate of $2 per day up to $400 (200 working days), without the need to track detailed expenses, calculate the size of the work space and will generally not request that employees provide signed paperwork by their employer. (UPDATE: An employee van claim $2 for each day you worked from home in 2020, 2021, or 2022 due to the COVID-19 pandemic, a maximum amount of $400 in 2020 and up to $500 in 2021 and 2022)

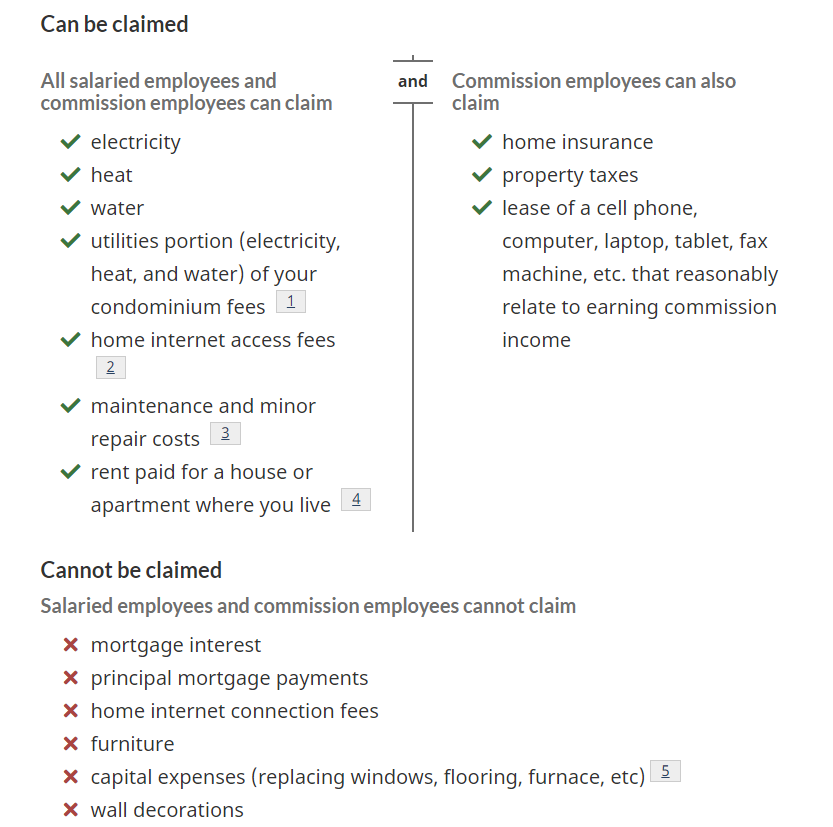

- You cannot deduct mortgage interest, property taxes, home insurance or motor vehicle expenses if you are claiming under the temporary flat rate method.

- The temporary flat rate method can be used to claim home office expenses paid by the employee including rent, electricity and home internet access fees, as well as office supplies like pens and paper, and cell phone minutes. You cannot deduct the cost of calculators, desks, filing cabinets as these are considered “capital expenses.”

- Employees with larger claims for home office expenses would have to use the existing detailed method to calculate their home office expenses deduction. CRA launched two simplified versions of the required tax forms (Form T2200S and Form T777S) and created an online calculator to help taxpayer in calculating the home office expenses.

- CRA has expanded the list of eligible home office expenses that can be claimed as work-space-in-the-home expenses to include reasonable home internet access fees.

For a more detailed information on working from home expenses visit Canada.ca/cra-home-workspace-expenses.